(Click to listen to the audio version)

Amid healthy increases in participation and play over the past several years, it isn’t uncommon to hear golfers in certain parts of the country lamenting greater limitations on tee time availability. Of course, this is very much dependent on supply and demand in a particular region, state or metro area.

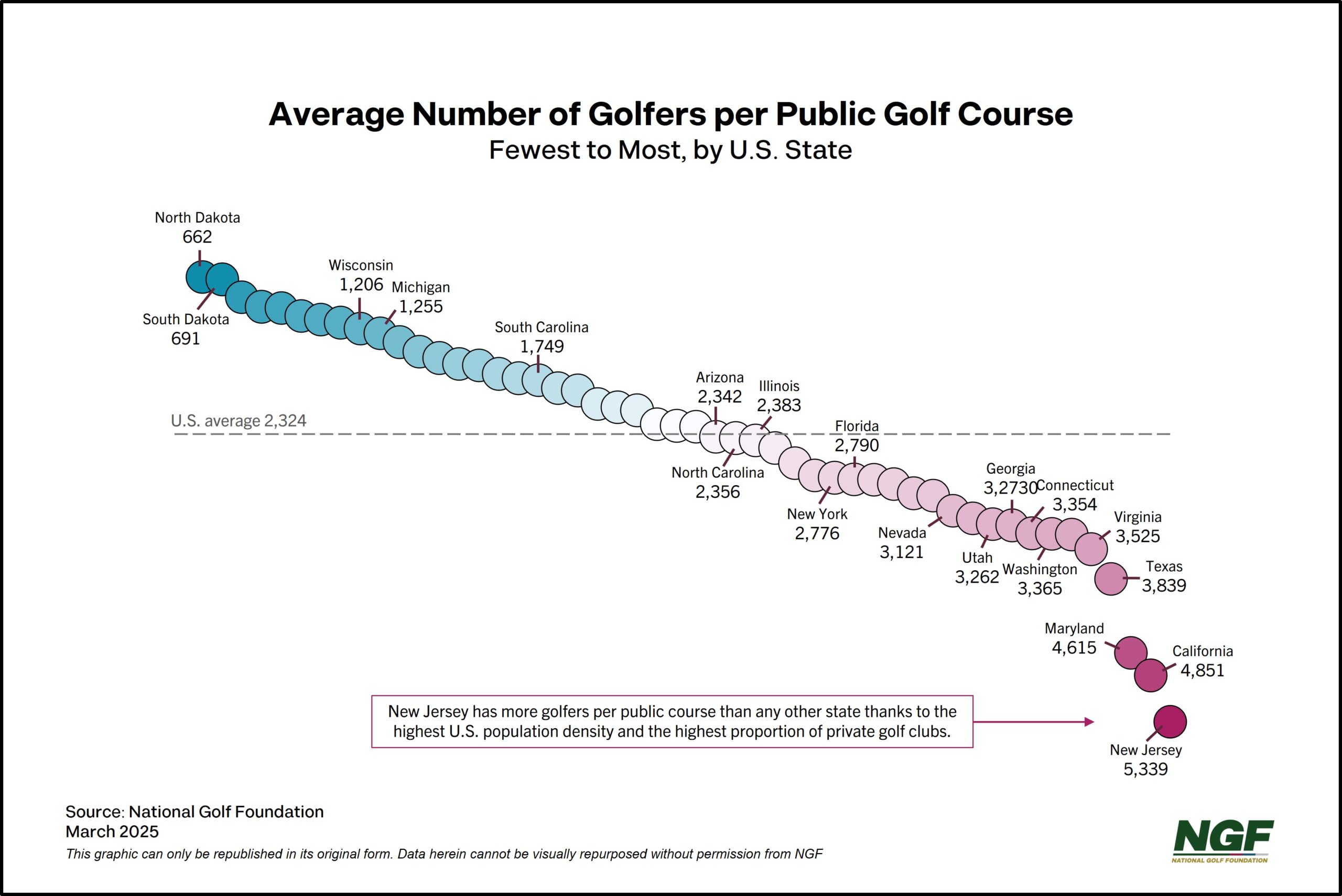

It begs the question of where public golf demand is at the highest levels?

The state with the most golfers per public course – New Jersey — is not only the most densely populated in the nation, but it is wedged between two of the most populous U.S. cities in New York (#1) and Philadelphia (#6).

In part because of its proximity to those metro areas, New Jersey has the highest proportion of private golf in any state. From heralded venues like Baltusrol, Ridgewood, Plainfield and Liberty National near NYC in the north to the world-renowned Pine Valley down south, almost half of New Jersey’s total golf supply is made up of private clubs, a departure from the national average of about 75% public. The result is a state that averages over 5,300 golfers for each of its 163 publicly accessible courses, just ahead of California – and particularly, the Los Angeles market.

Consider that New Jersey has almost 70 fewer public courses – daily fee, municipal or resort – than North and South Dakota combined, yet approximately three quarters of a million more resident golfers in total. It shouldn’t be too surprising that those coveted weekend morning tee times during peak season can be a bit harder to come by in North Jersey than North Dakota. Pricier too. And yet due to land values and limitations (NJ is the fourth smallest state), only two new public golf courses have opened in New Jersey over the past decade.

The supply looks considerably different as well.

While New Jersey has 27 public golf courses that are 9 holes in total, there are 168 courses in the Dakotas that are nine holes in length. North and South Dakota are among seven states that have more 9-hole facilities than the more typical 18-holers, a group that also includes Alaska, Iowa, Kansas, Maine and Nebraska.

Additional state-level statistics are now available in individual one-page member reports that detail golf supply, demand, rounds played, economic impact, and more.

Among the considerations for operators and golf businesses beyond better knowing their area:

- Pricing power implications

- Potential impact of no-shows

- Introduction and conversion challenges due to facility usage

- Awareness of focus on revenue maximization vs player experience

- Opportunity to run green-grass golf shops like golf retail stores in golfer-dense areas

- Consideration of how facility strain (turf, landscaping, infrastructure, clubhouses, technology, etc.) might be addressed in key markets

NGF members can access the new state one-pagers and other annual reports HERE.