( Click to listen to audio version)

Click to listen to audio version)

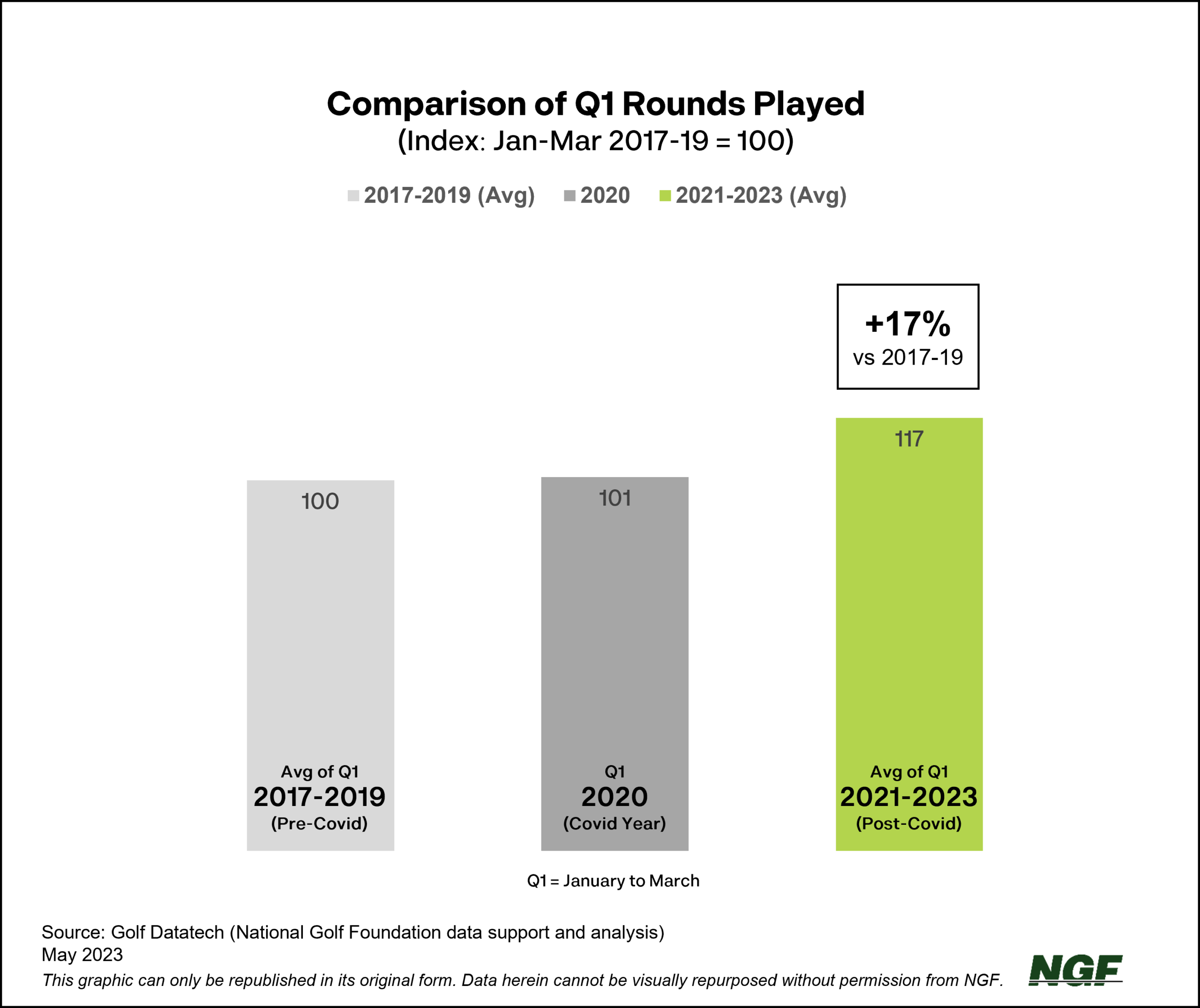

With Q1 rounds in the books and April research data starting to come in, it appears the pandemic demand surge continues to hold.

Comparing total January to March play for the past three years – post-Covid – rounds are up almost 17% compared to the three-year period ahead of the pandemic (2017-19).

Bear in mind that Q1 is notoriously inconsistent for golf, with play dictated by seasonality and the vagaries of the weather early in the year. Also, while January to March may account for a quarter of the calendar year, those months account for just over 16% of annual U.S. rounds.

On a state and regional level, weather impacts were the big Q1 story.

Consider California, which was hit by two successive atmospheric rivers in March alone and experienced one of the Top 10 wettest first quarters over the past 130 years. As a result, early season play was down 19% YOY in the state with the second-most golf courses in the country.

As a counter, there’s the Mid-Atlantic region, where early year play was up over 23% on average at the more than 1,600 courses in New Jersey, New York and Pennsylvania thanks to more favorable golf weather than Q1 of last year – most notably a surprisingly playable February. {click here to see related Spotlight sidebar story}

So far, the early returns on April play are positive. Many operators we’ve heard from so far indicate their rounds in April were up over last year.*

As always, though, it’s May through September that will be the real make-or-break period for the year. So, stay tuned.