Is this the beginning of the end? Of golf’s 15-year market correction, that is.

It might be.

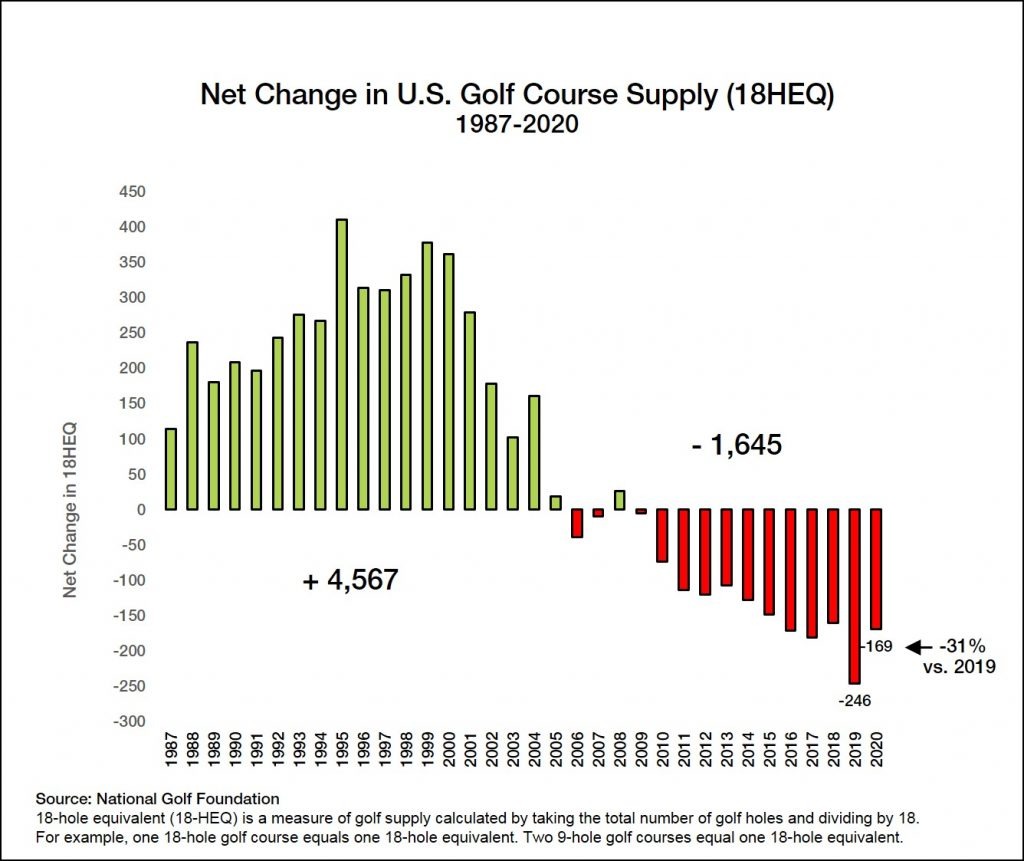

Last year, NGF recorded a net decline of 169 18-Hole Equivalent (18HEQ) golf courses – a 31% reduction from 2019’s 246, the largest drop on record. We ended 2020 with 13,362 18HEQs. (Two 9-holers equal one 18HEQ, meaning the total number of actual courses is higher; north of 16,000.)

The ongoing correction began in 2006, back when the real estate bubble began to deflate and a subprime mortgage crisis ensued. For the first time since Great Depression, the U.S. golf market finished the year with fewer courses than it started. Each year since, except 2008, the number of 18HEQs has fallen, with a total reduction of 1,645 (-11% from peak supply).

This followed a 20-year golf course development boom during which a total of 4,567 18HEQ courses was added to the nation’s supply (+44%). NGF was partly responsible. We issued a report with McKinsey & Co. in 1988 stating that golf course supply could become the limiting factor in golf’s growth if it didn’t keep pace with demand, which had been growing at roughly 4% on average for many years. The report advocated for the building of affordable, accessible public courses to support a greater number of golfers. Unfortunately, things didn’t go exactly to plan.

Our late 80s call for more courses brought residential real estate developers, entrepreneurs and even municipalities into golf with dollar signs in their eyes. NGF’s research was misinterpreted to mean that golf could not fail in any place and at any price. The laws of supply and demand went out the window, along with any feasibility studies that questioned the good business judgment of a developer.

In the late 1990s, golf demand plateaued. NGF issued another strategic report in 1999 urging the industry to return its attention to growing the number of golfers. About that time a young man with the initials ‘TW’ burst on to the scene, participation surged and the development boom marched on as the economy thrived. In the six years following this cautionary report, another 1,100 18HEQ courses were added (+8%). When the housing bubble burst, it led us into the deepest recession in history and the current correction in golf’s supply/demand balance.

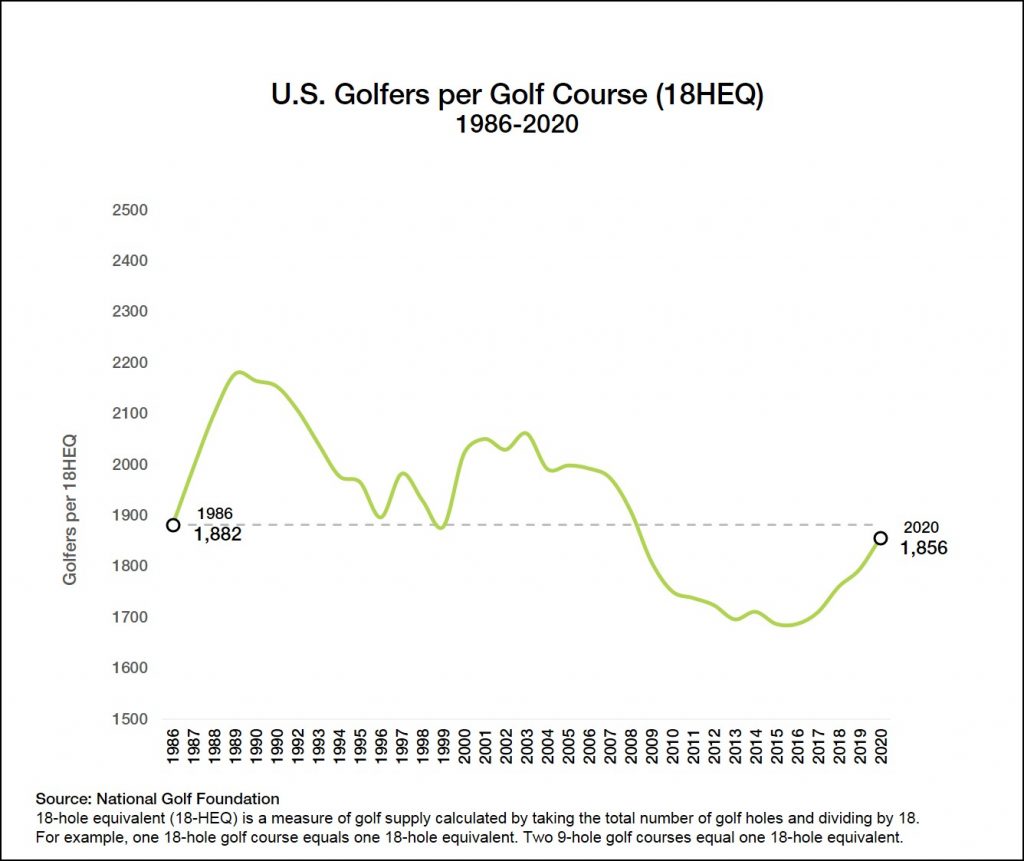

A decade and a half later, thanks partly to real estate developers hungry to turn unprofitable golf courses into profitable real estate, and a surprising surge in golf activity catalyzed by the pandemic, we are approaching equilibrium in supply and demand. After 2020’s participation bump, the number of golfers per 18HEQ now stands at 99% of what it was in 1986.

One of our recent facility studies revealed golf courses are in better financial shape today than they have been in years, which is good news for all of us in the golf business. Profitable golf courses are not just good for the game and business of golf, they’re essential. Profits allow owners to invest in the future and provide greater experiences for golfers.

Markets are always correcting and closures will continue in the U.S., especially given the demand for real estate. Like unemployment, course closures will never get to zero. Even during the 1985 to 2006 building boom, the U.S. averaged more than 40 18HEQ closures annually. If we double that number given the current market for land, that amount of churn is still less than 1% of overall golf supply.

All this being said, the U.S. market may have turned a corner on this correction. We’ll be tracking it closely.

And for those who remember NGF’s “course a day” mantra – mea culpa.