Golf’s Course Correction Is Over

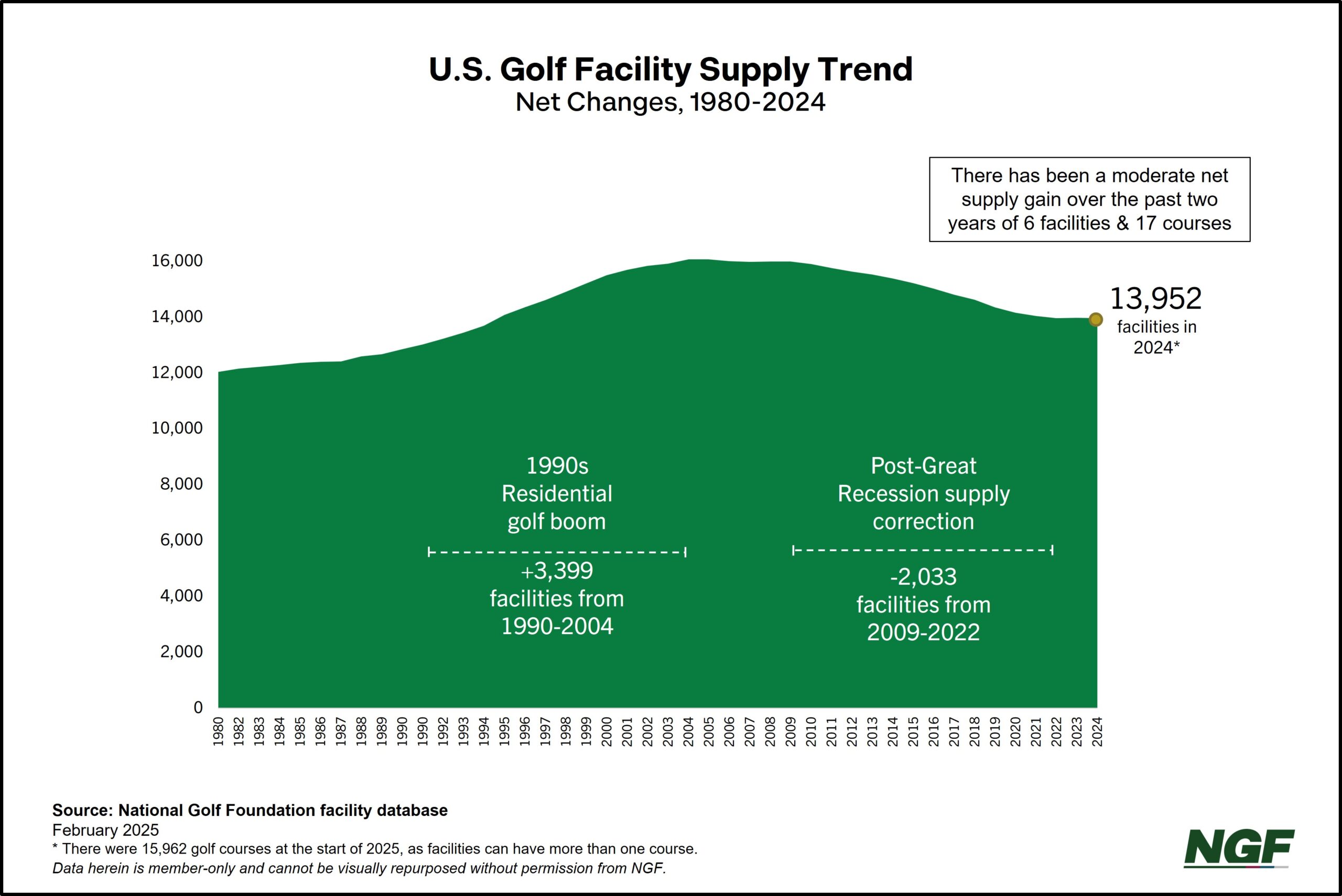

Over the past two years, the total number of open and operating golf courses in the U.S. has actually increased.

While that might not sound surprising to some given the game’s post-pandemic trajectory and notable participation and play gains in recent years, the reality is that the U.S. golf market – the best-supplied in the world – has undergone a substantial correction over much of the past two decades.

A perfect storm of conditions precipitated the rightsizing that began in 2006, when annual course closures first outnumbered openings.

The U.S. golf market had become oversaturated by the addition of more than 4,000 golf courses over a 20-year span from 1986 through 2005. That building boom was driven in large part by real estate, with many golf courses built to sell homes. When the U.S. housing bubble burst in the mid-2000s, the golf market followed, a correction accelerated by the Great Recession. Since 2006, over 2,000 facilities have been culled from the U.S. supply total.

But conditions have changed in recent years, with record play and on-course participation at its highest levels since the Great Recession hit. General facility health is drastically improved, and operators are investing in existing courses, including an increased number of renovations, reconstructions and resurrections. The number of annual course closures has decreased for five straight years, with the 2024 number of shuttered courses dipping to its lowest levels since 2004. Meanwhile, new course openings and development are both up.

As a result, since 2022 the net change in golf facilities is +6 and the course total is +17, inching total U.S. supply up from 15,945 to 15,962 courses. The ubiquity of golf exceeds that of one of the country’s leading chain restaurants, with more courses than McDonald’s locations nationwide. NGF members can click here to download the annual Golf Facilities in the U.S. report here for a deep dive into supply.

Given the demand for land, especially around urban areas seeking additional residential and commercial real estate, closures will continue to outpace openings in the years ahead. But for a more holistic view of supply, our researchers also look at re-opened courses, i.e. facilities that undertook a renovation or a reconstruction that shut down operations, whether for a short period or an extended stretch. Resurrections are a newer category, an example being a course that’s been closed for more than a year but is given new life, most frequently following an ownership change. When factoring these kinds of investment, the net change in annual supply has been minimal for the past couple years.

The current momentum suggests the trend in supply stability has legs.

This balanced state is an indication the industry has matured beyond its boom-and-bust cycle into a more sustainable phase of measured growth, though this equilibrium doesn’t eliminate the need for courses, operators and related businesses to continue focusing on strategic positioning and evolving with changing consumer preferences.

CLICK FOR GOLF FACILITIES IN THE U.S. REPORT

National Golf Foundation

Short Game.

"*" indicates required fields

How can we help?

NGF Membership Concierge

"Moe"

Learn From NGF Members

Ship Sticks Secrets to a Hassle-Free Buddies Golf Trip

Ship Sticks Secrets to a Hassle-Free Buddies Golf Trip

Whether you’re the head planner of your upcoming buddies golf trip or simply along for the ride, we’ve gathered a few easy ways to keep everyone in your group happy.

Read More... Golf Course Turf, Soil and Water Quality Diagnostic Testing

Golf Course Turf, Soil and Water Quality Diagnostic Testing

As humans, we see our primary care physician on a regular basis to proactively evaluate our vital signs. Likewise, a superintendent should perform frequent diagnostic testing on their golf course.

Read More... Unlocking Distance: Launch Conditions and Angle of Attack

Unlocking Distance: Launch Conditions and Angle of Attack

We’ve long known that higher launch and lower spin is a powerful combination for generating consistently long and straight tee shots. A key factor in optimizing launch conditions, one often overlooked, is ...

Read More...